Weekly Market Insights 12.30.24

A New Beginning

Financial Markets

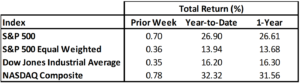

This past week was a disappointing one for equity markets. The major market indices opened the week on a strong note but faltered as the week went on. It will be interesting to see what the last trading week of the year brings.

Looking at equity returns for 2024, readers will quickly see why investors should be quite satisfied with the year as a whole. Still, some may be wondering why we are witnessing year-end weakness. There are, of course, many possible reasons—lofty valuations, fear of political dysfunction, and year-end rebalancing, to name a few. In reality, the weakness can probably be explained by a combination of factors, all magnified by the hawkish takeaways from the December Fed meeting. It is reasonable to assume the latter has been the dominant factor. The Federal Reserve and interest rates continue to dominate the investing landscape.

Economics

The global economy is at a fascinating crossroads. In the United States, economists and investors wonder whether the economy is too strong for further Fed easing. Investor concerns only intensified after Fed officials signaled fewer rate cuts going forward at their final meeting of the year. Looking abroad, most other economically developed countries remain in slow growth mode. The exception, of course, is China, which is experiencing more serious economic difficulties.

We remind investors that it is the duty of the Federal Reserve to remain diligent with their monetary policy decisions to promote price stability. At present, their main focus is to prevent a second wave of inflation. Therefore, the harsh political rhetoric about tariffs, tax cuts, and deportations raises a red flag concerning future inflation. There remains considerable uncertainty around exactly what the incoming administration’s economic policies will be. What is economic policy and what is political rhetoric remains to be seen. So, a wait-and-see posture is most likely the best path to follow.

A few months ago, we began writing about a very positive economic outcome that may be in the cards for the United States. We boldly dubbed it the next industrial revolution. This premise is based on the power of increasing productivity, and there are reasons to believe the United States may be on the verge of a productivity boom. What will it take to accomplish this, and where do we stand? Well, it will take a boost in entrepreneurship, accompanied by a willingness of businesses to deploy available capital towards efficiency-boosting technologies. We will also need to divert more resources towards education to avoid a skills mismatch between the labor force and the new jobs these technologies will bring. Vast numbers of business licenses have been issued, and many U.S. businesses have made substantial capital investments in AI and quantum computing. There will undoubtedly be pushback, as changes of this magnitude can be frightening.

Conclusion

We expect a considerable amount of confusion as the new administration takes shape. It may take longer than usual to gain a level of comfort because so many members of the incoming administration will be new to government service. We do not expect dramatic changes in the economy in the immediate future, although financial markets may be a bit volatile due to the new president’s tendency towards hyperbole. As we enter the new year, we are holding out hope that our idealistic outcome can become a reality. However, this brave new world cannot happen without private/public cooperation. It will be well worth it! Remember Paul Krugman’s famous remark, “Productivity isn’t everything, but in the long run, it’s almost everything.”

Read pdf here.