Women & Wealth: Expect the Unexpected

The time is now to take control of your finances.

A life-changing event will not wait until we are prepared.

As the pandemic continues to create uncertainty, financial planning is more important than ever, especially for those who have been disproportionately impacted.

Women have long faced particular challenges including outsized financial and caregiving responsibilities, longer life expectancies, more career interruptions, and other disruptions. While economic opportunities have improved in recent years for women, the pandemic has created setbacks for many.

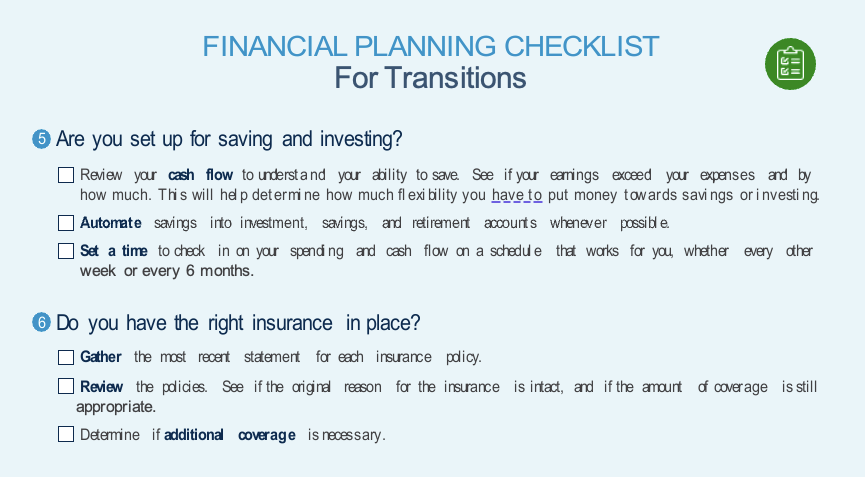

Here you will find a checklist that can be helpful for unexpected events or transitions from one situation to another. We also offer our thoughts on why it is important to account for the specific needs of female clients in the planning process.

Women are far more likely than men to consider leaving the workforce in the wake of the COVID-19 crisis.1 More women have been laid-off or furloughed compared to men. Black women and women of color are even more severely impacted professionally, in addition dealing with the heavier toll that COVID-19 has taken on their communities.2

These setbacks can cost years of progress for women professionally and financially, threatening long-term financial security and independence.

A bold and adaptable financial plan is critical as the foundation to rebuild, pivot, or recover from a distressing event.

It’s important to understand the key factors that help explain why women are at greater risk of forfeiting financial security when dealt an unexpected change:

- LONGER LIFE EXPECTANCIES

It is especially important for women to account for their lifespan in planning for their financial future. Even a couple of additional years carry large implications on expenses, including health care and long-term assistance. For those living with a long-term partner or family member, there are additional impacts of shouldering a greater portion of housework and physically caring for someone else. For many women, realistically assessing the likelihood of longevity and the associated physical, financial, and emotional costs can be the difference between living on your own terms or in dependency.

- PERSISTENT PAY GAP AND CAREER INTERRUPTION

Women make 82 cents for every dollar paid to men,3 and time they spend out of the workforce keeps their salaries low. This has other implications including lower Social Security benefits and slower debt payment. The improvement to women’s earnings ratio varies greatly by race, with Black and Latina women remaining at the same gap rate for the past 30 years with no improvement when they attain higher education.4

- SOLO LIVING

The odds are extremely likely that a woman will live alone at some point in her life.5 Divorce rates have been rising sharply, contributing to this trend. Adults over 50 lead other age groups in the rate of increase in divorces, doubling since the 1990s.6 “Gray divorce” is particularly problematic for women, who are far more likely to face economic insecurity. Widowers in the same age group, on the other hand, are the most advantaged singles.7 Whether by divorce or death, women are far more likely to find themselves suddenly single, and at a disadvantage.

- UNDERSERVED BY FINANCIAL INSTITUTIONS

Despite the recent economic impacts of COVID-19, the growth of women’s wealth is projected to outpace global wealth growth over the next few years.8 Women may have better opportunities than ever before to grow and accumulate wealth. However, possessing money today does not guarantee lasting wealth and financial security. Access to resources, education, and advisors is the beginning of a reliable financial foundation, and these very building blocks have not been available to women in the same way they have been for men.

Everyone should have a financial plan, but the urgency for women and the impact it will have cannot be overstated.

OUR PLANNING APPROACH

While we cannot predict and prevent all the possible changes you will face, we draw upon our deep expertise and decades of experience to equip you with a financial plan that is honest, resilient, adaptable, and most importantly, wholly yours.

The process is simple, but the application is critical.

1. Understand Your Financial Picture

We review your current financial picture with you to establish a starting point and understand your priorities. We have tools that can help with this, including a full questionnaire, a financial planning checklist to identify strengths and gaps, and a budget worksheet to assess your spending needs.

2. Develop Your Plan

Once we understand your current situation and your objectives, we can work together on developing a plan. This is a partnership where we establish your “baseline” scenario, or a projection if you stay the current course.

From here, we work together to identify ways to make the plan more solid and durable across a wide range of possibilities. We look for vulnerabilities in the plan that can be shored up to lower the chance of future surprises.

Alternate scenarios provide insight to the impact of decisions, from big life decisions to small adjustments such as moving to a different state, retiring earlier or later, donating to charity over your lifetime or in your estate planning.

3. Monitor and Adapt

Once you have a financial plan in place, keeping it up-to-date is key. We will review the assumptions in your plan on an ongoing basis to ensure it remains relevant. The good news is having the framework in place helps tremendously if the unexpected happens. You do not have to start from scratch—you already have a framework.

A STARTING POINT

Thoughtful planning and preparation is our best guard against the unexpected, and could be the difference between a temporary setback and long-lasting financial damage.

The checklist on the following page can help you get started if you are facing changes, or serve as a general financial health check-up.

Take charge of your finances and your future.

Our Transitions Checklist serves as a starting point for a more comprehensive review of your financial situation. Please use additional 1919 tools to help you in your financial planning journey:

At 1919 Investment Counsel, we serve our clients by listening, learning, and responding to their needs. This enables us to develop practical, actionable plans in collaboration with our clients. We are committed to listening before we prescribe and apply our deep expertise to help our clients plan for their future and navigate difficult times.

Take control of your financial future, before the unexpected occurs.

FOOTNOTES

1 McKinsey Blog, “How are working women doing during COVID-19?” September 2020. https://www.mckinsey.com/about-us/new-at-mckinsey-blog/how-are-working- women-doing-during-covid-19-our-women-in-the-workplace-study-explores

2 McKinsey Insights, “Women in the Workplace 2020,” September 2020. https://www.mckinsey.com/featured-insights/diversity-and-inclusion/women-in-the- workplace

3 American Association of University Women (AAUW), “The Simple Truth About the Gender Pay Gap, 2020 Update.” https://www.aauw.org/resources/research/ simple-truth/

4 AAUW, “Race and the Pay Gap.” https://www.aauw.org/resources/research/race-and-the-pay-gap/

5 According to a UBS survey, 8 out of 10 women will be alone at some point in their lives. https://www.ubs.com/us/en/investor-watch/own-your-worth.html

6 Pew research, “Led by Baby Boomers, divorce rates climb for America’s 50+ population.” March 2017 https://www.pewresearch.org/fact-tank/2017/03/09/ led-by-baby-boomers-divorce-rates-climb-for-americas-50-population/

7 Sage Journals, “Marital Biography, Social Security Receipt, and Poverty,” Lin, Brown, & Hammersmith. December 2016. https://journals.sagepub.com/ doi/10.1177/0164027516656139

8 BCG, “Managing the Next Decade of Women’s Wealth,” Zakrzewski, Newsom, et al. April 2020 https://www.bcg.com/publications/2020/managing-next-decade- women-wealth.aspx\