Weekly Market Insights 10.30.23

A Speaker is Elected, GDP Grows, and Equities Fall

Financial Markets

There were several major developments last week. At long last, the House of Representatives elected its Speaker, the first preliminary reading for 3rd quarter GDP indicated that the economy is moving ahead at a good clip, and the market correction continued. Of course, that’s far from the whole story. Investors are currently faced with two wars, neither showing signs of near-term resolution. Inflation fears have not subsided, and, although a Speaker has been elected, he is a relative unknown, even to some of his colleagues in the House. As we mentioned, the equity market correction continued through the week. There was a rally attempt earlier in the week, but that ultimately failed to translate into durable gains. For the week, the Dow fell by 2.14%, the S&P 500 by 2.53%, and the NASDAQ by 2.62%. There are a number of reasons markets have been unable to sustain a rally, and we expect to see further weakness until there is less uncertainty over the future of the economy.

Economics

Market participants were happy to see the House finally elect a Speaker. The next question for many is likely, who is Mike Johnson? Here are a few highlights. He is a representative from Louisiana and is 51 years old. He is well spoken and seemingly pleasant. His early acceptance speech was calm, absent of harsh rhetoric, and he did speak of compromises. Since his election to Congress in 2016, he has made his mark by advancing conservative positions on cultural issues. He was four-square behind the movement to overturn the 2020 election. He now qualifies that? Last, and perhaps most important, is the question of leadership. Representative Johnson has never held a leadership position in the House and has never been a committee chair. He is coming in at a difficult time. In any case, his demeanor and comments are encouraging, and he certainly deserves every chance for success. Almost irrespective of policy, it should be a relief to investors to finally see progress on some of the open issues.

On Wednesday, all eyes will be on the Fed. Fed officials have already indicated that they will likely hold rates steady, but investors will try to read the tea leaves to see if there will be further tightening in the future. It seems unlikely that this meeting will be anything but ambiguous. It is really interesting to consider the dynamics of the current economic situation. The Fed has been raising interest rates, inflation appears to be slowing, and economic growth is accelerating. Consumer spending, the main driver of economic growth, is strong and increasing. According to the University of Michigan’s consumer survey, consumers are feeling somewhat less secure in their jobs, but their biggest fear has been, and remains, inflation. Perhaps this last point is one of the pieces to the puzzle. Even with rising rates, consumer spending has been strong. Macro 101 tells us that consumers, in times of inflationary pressures, will spend quickly in an attempt to get ahead of inflation, which may help to explain the strong economic growth we are seeing now. Perhaps the answer is more simple, and Chairman Powell has been correct in saying that rates haven’t been in restrictive territory long enough.

Conclusion

Confusion reigns supreme! There are so many moving parts that one is tempted to throw up one’s hands and give up. Joanne W. Hsu, Director of the University of Michigan’s Consumer Sentiment Survey, made a good observation when she said, “The polarization of politics and an unrelenting 24-hour news cycle with the internet and cable may have something to do with it… Consumers hear more bad news about inflation than they did in the past.” We have written a lot about change, but we urge readers not to think that these changes are permanent. Most are related to the pandemic and its interruption of the normal economic and business cycles.

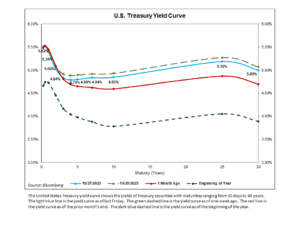

Yield Curve Update

Read pdf here.